The Strait of Hormuz is now officially closed again. (Writing at 10:40CET)

Despite many headlines, as well as Trump’s statements, to the contrary, the de-facto situation on the water is that the Strait of Hormuz is not fully open as of 06:00 CET Saturday morning.

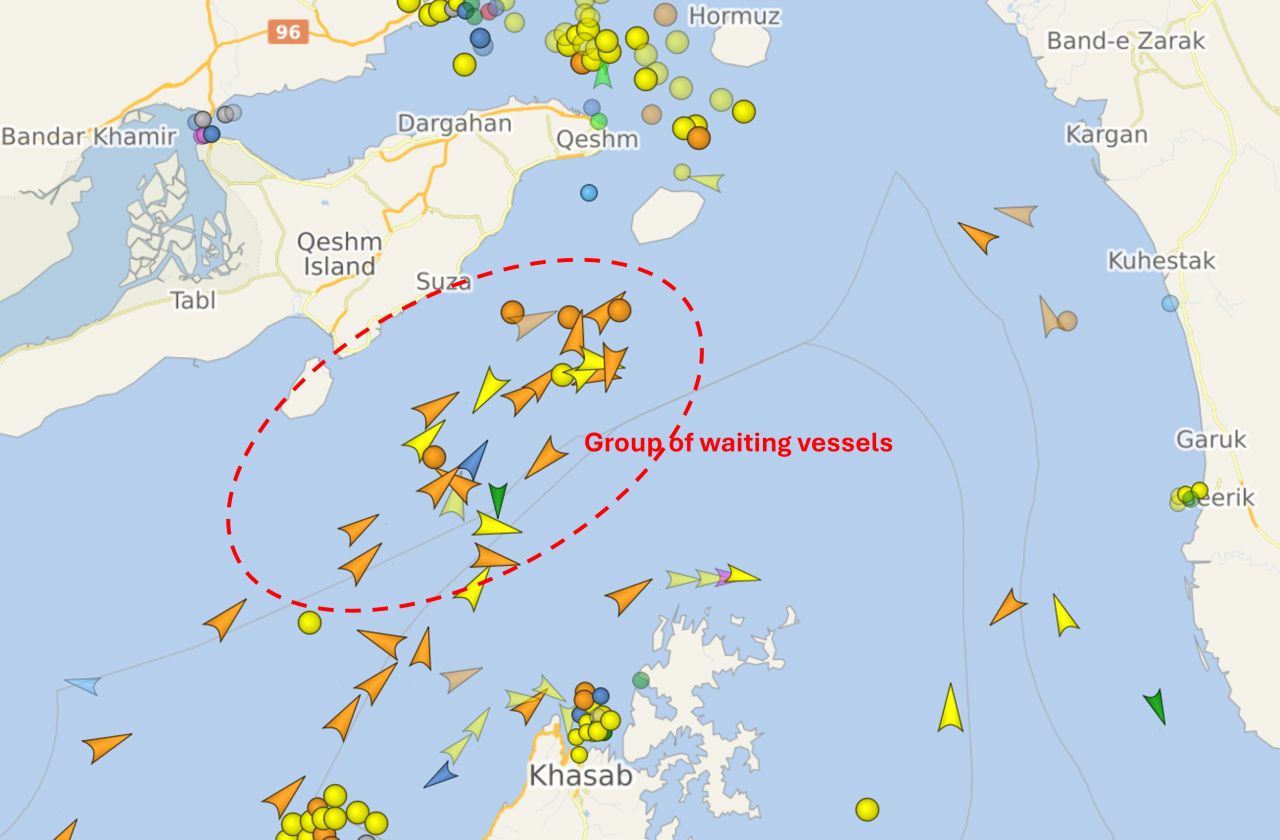

Immediately following the statement yesterday that the Strait was open, dozens of vessels began sailing towards an exit from the Persian Gulf.

However, this exodus armada almost all stopped short of actually exiting. Presently we see more than 30 vessels now in a holding pattern waiting for the final crossing as shown in the image below.

For container vessels, CMA CGM was quick to also set sail, and they have 4 of their vessels in this group of waiting vessels.

Only very few vessels made the transit, including the empty cruise vessel "Celestyal Discovery".

The issue appears to be conflicting messages from Iran and the US. The Iranian message was that the strait was open, but you still had to coordinate with their Navy for passage. They also stated that they would close the Strait again if the US upheld the blockade against Iranian ports. The US have stated they are indeed upholding the blockade.

(Update 09:30 CET: an increasing number of the waiting vessels are now crossing Strait of Hormuz)

The freight rates for futures contracts are inching slightly upwards for Asia-N.Europe. The index shown by NYSHEX for futures on the Intercontinental Exchange (ICE) shows Asia-N.Europe rates moving slightly upwards to an apex of 2700 USD/40’ in May and 2900 USD/40’ in June versus a present level just above 2200 USD/40’. But after this point the futures rate declines towards a low of 2600 USD/40’ in October.

Pacific rates show a very different futures development. Both coasts see steadily rising rates until a peak in November. USWC rates are set to increase to 2850 USD/40’, 570 USD higher than the present level. USEC rates are set to increase to 3550 USD/40’, 500 USD higher than the present level.

As always it should be noted that this reflects a market assessment of where buyers and sellers see a reasonable level for hedging the risk of price movements up or down. In other words, the current weakness in spot rates has not eliminated a concern of modest rate increases in the coming months.

Global average bunker fuel prices continue to slowly decline. They remain highly elevated compared to pre-crisis, but are now at the lowest level seen since March 10th.

Another request from Maersk to be able to change rates on US trades with less than 30 day notice was denied by the FMC.

Today is day 881 of the Red Sea crisis and day 50 of the Hormuz crisis.